Question1: A disgruntled customer claims that he should not have to settle an FRA with you because it is really just a wager. What type of risk are you exposed to?

Question2: By what means should a financial institution preferably submit SSI changes and notifications to its clients?

Question3: What rate should be used if the settlement date in a foreign exchange transaction is no longer a "good" date?

Question4: You are quoted the following market rates:

Spot USD/JPY 123.65

1M (30-day) USD. 2.15%

1M (30-day)JPY 0.10%

What is 1-month USD/JPY?

Question5: A dealer does the following deals in EUR/USD:

buys EUR 1 m at 11020

sells EUR 3 m at 1.1022

buys EUR 2 m at 1.1002

buys EUR 1.5 m at 1.1012

What position does the dealer now have?

Question6: How would you delta hedge a deeply "in-the-money" short put option?

Question7: A customer would hedge a currency exposure with a forward FX time option if:

Question8: When dealing with customers, financial market professionals are advised by the Model Code to clarify that all transactions are entered into solely at each partys risk by explicitly agreeing in writing that:

Question9: You and a dealer at another bank have an informal bilateral reciprocal arrangement to quote each other two-way prices. During periods of high volatility, the other dealer refuses to quote to you. The Model Code states that

Question10: The seller of a floor:

Question11: Confirmations must be sent out

Question12: What should be done if a broker fails to conclude a transaction at the quoted price and the dealer has to accept a lesser quote to neutralize his risk?

Question13: Your broker quotes you EUR/USD at 1.3425-28. You respond by saying "yours". Which one of the following statements is true?

Question14: Which of the following will tend to have the lowest yield?

Question15: When considering interest rate risk in the banking book, retail demand deposits without fixed contractual maturity:

Question16: What recommendation does the Model Code make in cases of market disruption?

Question17: What does the Model Code advise regarding the taping of telephone conversations?

Question18: If EUR/USD is 1.1025-28 and the 6-month swap is 112.50/113, what is the 6-month outright price?

Question19: Which of the following is sometimes called two-name paper?

Question20: Under which circumstances are banks allowed to park positions with a counterparty?:

Question21: What does the Model Code say about omitting the "big figure" in voice communication?

Question22: Your GBP/CHF rate is 1.3710-15. How many GBP would your customer have to give you to buy CHF

10,000,000.00?

Question23: Which of the following is not an officially published settlement or reference rate?

Question24: Which of the following statements is correct?

Question25: When may a broker assume a deal is closed?

Question26: If I say that I have "bought and sold" EUR/USD in an FX swap, what have I done?

Question27: What is the result of combining a 1-month buy and sell FX swap with a 2-month sell and buy FX swap?

Question28: What is the value date of a 1-month outright forward FX transaction dealt today, if today's spot date is Monday, 30th January? Assume there are no bank holidays and that the year is not a leap year.

Question29: An option granted by the seller that gives the buyer the right to enter into an underlying interest rate swap transaction is ca lied:

Question30: Lending for 3 months and borrowing for 6 months creates a 3x6 forward-forward deposit. The cost of that deposit is called:

Question31: The process of confirming trades is a function that can be performed by:

Question32: Where there are shared management responsibilities or where an investment or shareholding exists in a broker by a counterparty:

Question33: The use of standard settlement instructions (SSI's) is strongly encouraged because:

Question34: Where dealing for personal account is allowed, what safeguards to prevent abuse or insider dealing are stated by the Model Code?

Question35: What needs to be done in the event that a trade is amended by one or both parties?

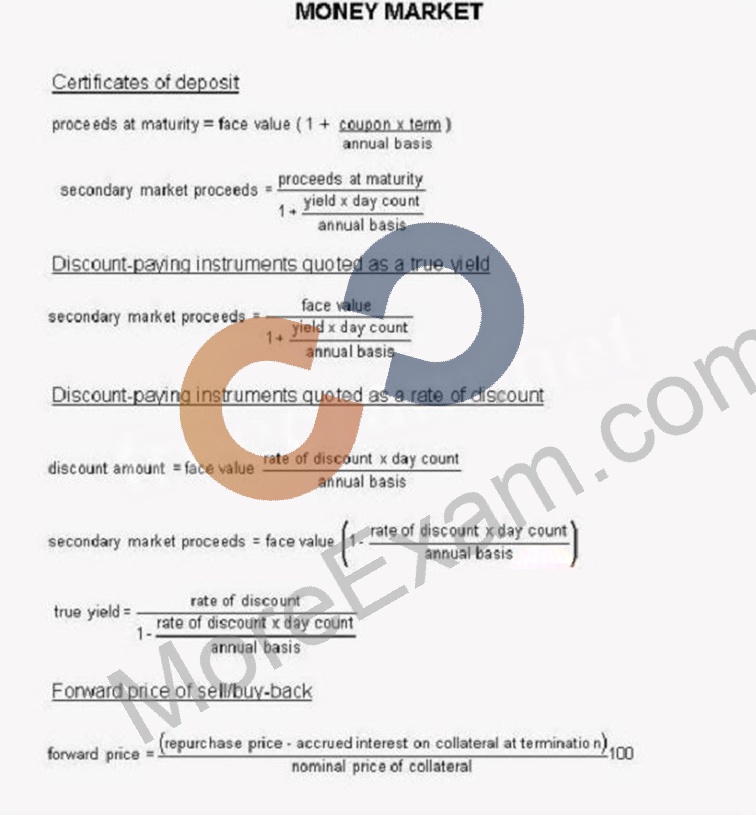

Question36: Click on the Exhibit Button to view the Formula Sheet. A 6-month (182-day) investment of CHF15.5 million yields a return of CHF100,000. What is the rate of return?

Question37: Which one of the formulae below is correct?

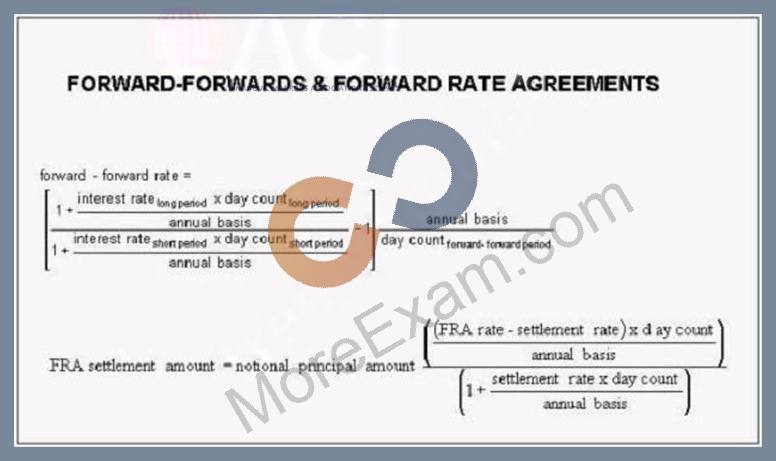

Question38: Today is the fixing date for a 6x9 FRA that you sold at 2.55%. BBA LIBOR fixes at 2.7175%.

Which of the following is true?

Question39: What is the Repurchase Price of a classic repo?

Question40: In the event that standard settlement instructions are provided by a third party, full authentication and authorization of those SSIs should be independently performed by?

Question41: The Model Code recommends that standard terms and conditions be used in legal documents. Which one of the following statements is correct?

Question42: Cable is quoted at 1.5575-80 and you say "5 yours!" to the broker. What have you done?

Question43: Which of following is not true?

Question44: If 6-month EUR/AUD is quoted at 29/32, which of the following statements is correct?

Question45: A 3-month (90-day) USD deposit is 5.5625% and 6-month (180-day) USD deposit is 5.75%. What is the

3x6 USD deposit rate?

Question46: The risk associated with a stock or a bond that is not correlated with events in the market is known as:

Question47: Which of the following statements is true?

Question48: After having quoted a rate of 1.5005-10, the quoting bank says, "Your risk". This means:

Question49: A 1-month (30-day) USCP with a race value of USD 5 million is quoted at a rate of discount of 2.31%. How much is the paper worth?

Question50: You are entering into a swap as a fixed rate receiver with Party A and into an offsetting position with party

B. All other things being equal, which of the scenarios below will lead to the greatest increase in the sum of the Credit Value Adjustments for A and B?

Question51: Purchasing a USD/JPY call option is equivalent to:

Question52: You and a dealer at another bank have a verbal bilateral reciprocal arrangement to quote each other two- way prices. During periods of high volatility, the other dealer refuses to quote to you. What does the Model Code say about this situation?

Question53: Issues relating to the bank's liquidity management are commonly discussed in:

Question54: Spot cable is quoted at 1.6048-53 in the brokers and you quote a customer 1.6050-55 in USD 3 million, If they sell USD to you, how much GSP will you be short of?

Question55: Under Basel rules, what is the meaning of LGD?

Question56: Under the Model Code, if a broker shouts "done" or "mine" at the very moment a dealer shouts "off":

Question57: The primary issue for insuring prudent liquidity management in accord with the guidance provided by the Basel Committee (Basel II I Basel III) is:

Question58: 7-day USCP is quoted at a rate of discount of 1.75%. What is its true yield?

Question59: You are quoted the following rates:

Spot EUR/NOK 7.5250-60

O/N EUR/NOK swap 3.10/3.20

T/N EUR/NOK swap 3.12/3.22

S/N EUR/NOK swap 9.35/9.55

At what rate can you sell EUR against NOK for value tomorrow?

Question60: If the issuer of the collateral used in a repo defaults during the term of the transaction, who suffers the loss?

Question61: What should be done when a voice broker hits a dealer's price as "done" at the very instant the dealer calls

"off"?

Question62: When is a broker allowed to assume a deal is closed:

Question63: A bank expects interest rates to fall with a parallel downward shift in the yield curve. What action should the bank take, if it wants to benefit from this view?

Question64: Which of the following is not transferable?

Question65: Click on the Exhibit Button to view the Formula Sheet. You are short of 6 Dec euro dollar futures contracts at 98.10. Yesterday, the closing price was 98.15. Today's closing price is 97.905.Whatvariation margin will be due?

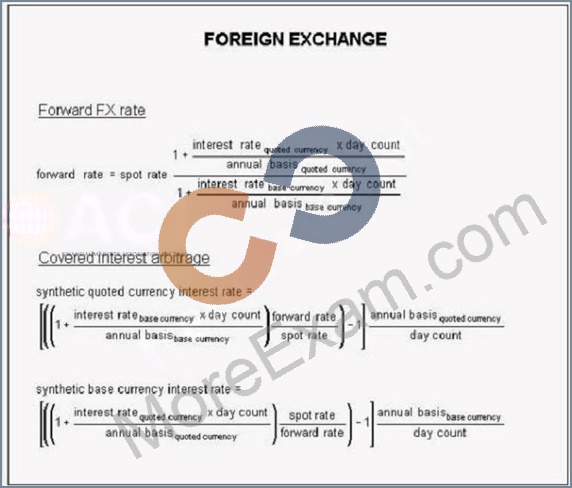

Question66: The Interest Rate Parity Theorem should work because, when one sells a low interest rate currency to invest in a high interest rate currency and hedges the currency risk:

Question67: The delta of an option is:

Question68: The buyer of a currency put option has:

Question69: Which of the following does not represent an operational risk as defined by Basel rules?

Question70: A purchased 3X6 FRA should be reported in a gap report as

Question71: Which of the following is not the responsibility of the asset and liability committee (ALCO)?

Question72: What happens when the issuer of a bond being used as collateral in a classic repo fails to pay a coupon on the bond during the term of the repo?

Question73: Fraud is typically classified as:

Question74: What is the minimum basis on which a BCP should be updated and tested?

Question75: Where answer phone equipment is used for reporting and recording of off-premises transactions, it should be:

Question76: What is the policy of the Model Code on drugs, alcohol and other substance abuse in the dealing room?

Question77: Which position below is NOT a component of common equity Tier 1 capital?

Question78: What does the Model Code recommend with regard to any give-up agreement between a prime broker and an executing dealer?

Question79: Where internet trading facilities are established by a bank for a client, the conditions and controls should be stated in a rulebook produced by:

Question80: Which of the following statements best describes the conditions under which a prime broker may accept a trade given up?

Question81: Under Basel rules the risk weight for MA-rated claims on corporate in the standardized approach

Question82: A 3-month (91-day) UK Treasury bill with a face value of GBP 50,000,000.00 is quoted at a yield of 4.25%.

How much is the bill worth?

Question83: For which one of the following disputes is the Chairman and members of the ACI's CFP ready to assist through the ACI's Expert Determination?

Question84: Which of the following would not constitute an event of market isruption under the Model Code?

Question85: How much is one big figure worth per million of base currency if EUR/GBP is 0.8990?

Question86: In a dispute between the dealer and a broker, the Model Code recommends that this should be referred in the first instance to:

Question87: You quote a price to a broker on EUR 100 million. Your price is hit for EUR 50 million. What does the Model Code say about this situation?

Question88: What is a long strangle option strategy?

Question89: Dealers are authorized to deal:

Question90: Which of the following are quoted in terms of a yield-to-maturity?

Question91: You hear from several counterparties that a major market participant has taken major losses on long USD/ JPY positions. You know the reports are untrue, as you have in fact bought large amounts of USD/JPY from that very firm, which means that the impact of the reports on the market would be helpful to your position.

Question92: As regards controls, which of the following best practices for counterparty identification is incorrect?

Question93: Which one of the following statements concerning covenants is incorrect?

Question94: You have borrowed at 3-month LIBOR+50. LIBOR for the loan will be re-fixed in exactly one month. The market is quoting:

1x3 USD FRA 0.42-45%

1x4 USD FRA 0.54-58%

1x5 USD FRA 0.57-62%

To hedge the next LIBOR fixing, you should:

Question95: The Interest Rate Parity Theorem states that:

Question96: Today's date is Thursday 12th December. What is the spot value date? Assume no bank holidays.

Question97: Click on the Exhibit Button to view the Formula Sheet. Bank A pays for EURO 5 m at 1.1592. Bank B offers EURO 10 m at 1.1597. Broker XYZ quotes to the market EURO /USD 1.1592/97. Bank C takes the offer at

97. The broker is obliged to reveal:

Question98: The one-month (31-day) GC repo rate for French government bonds is quoted to you at 3.75- 80%. As collateral, you are offered EUR 25,000,000.00 nominal of the 5.5% OAT April 2015, which is worth EUR

28,137,500.00. If you impose an initial margin of 1%, the Repurchase Price is:

Question99: If a dealer has interest on one side, and the other side is dealt away, the broker should:

Question100: When dealing with a fund manager, who will allocate shares in a transaction to his unknown clients after the transaction has been executed with you, you should:

Question101: A prime broker may not reject a trade given up if:

Question102: A Eurozone-based bank that is liability-sensitive to market interest rate changes might reduce interest rate risk by:

Question103: Which of the following situations would be most likely to result in a negative mark-to-market for a bank borrowing short term and lending long term?

Question104: Using the following rates:

3M (90-day) EUR deposit 0.25%

6M (180-day) EUR deposit 0.50%

What is the rate for a EUR deposit, which runs from 3 to 6 months?

Question105: What is the correct interpretation of a EUR 5,000,000.00 one-week VaR figure with a 99% confidence level?

Question106: A fixed rate forward/forward non-deliverable deposit/loan transaction, settled in cash with an agreed upon process for calculating the market reference at the commencement of the forward/forward period, is called:

Question107: With reference to dealing periods, what does the term "short dates" refer to?

Question108: You have a USD loan that is priced at 3-month LIBOR+50. LIBOR for the loan will be re-fixed in exactly one month. The market is quoting:

1x3 USD FRA. 1.95-98%

1x4 USD FRA. 2.07-10%

1x6 USD FRA 2.25-28%

To hedge the next LIBOR fixing, you should:

Question109: What is the day count/annual basis convention for JPY money market deposits?

Question110: You are short of 6 December EURODOLLAR futures contracts at 99.50. Yesterday, the closing price was

99.35. Today's closing price is 99.105. What variation margin will be due?

Question111: Which of the following may pay a return as a mix of income and capital/gain loss?

Question112: Using the following rates:

3M (90-day) eurodeposits3.50%

6M (180-day) eurodeposits3.75%

What is the rate for a deposit, which runs from 3 to 6 months?

Question113: What is the purpose of a long strangle option strategy?

Question114: What is the name of the reference against which most USD and JPY deposits and loans are fixed in London?

Question115: Where voicemail equipment is used for the reporting and recording of off-premises transactions, voice mail should be:

Question116: Which of the following transactions would have the effect of shortening the average duration of liabilities in the banking book?

Question117: If GSP/USD is quoted to you at 1.61 20-30, how much GSP would you receive if you sold USD 2000,000?

Question118: What is the meaning of CCP within the Basel framework?

Question119: The two-week repo rate for the 5.25% Bund 2011 is quoted to you at 3.33-38%. You agree to reverse in bonds worth EUR 266,125,000.00, but insist on an initial margin of 2%. You would earn repo interest of:

Question120: Where the matter of dealing for personal account is concerned, the Model Code recommends that

Question121: You buy a 181-day 2.75% CD with a face value of USD 1,500,000.00 at par when it is issued. You sell it in the secondary market after 150 days at 2.60%. What is your holding period yield?

Question122: Bank B's price is shown by a broker to Bank A and is dealt by Bank A.

If Bank A wants to increase the amount of the transaction, what is good market practice according to the Model Code:

Question123: EURIBOR is the:

Question124: You are quoted the following rates:

Spot cable 1.5340-43

0/N cable swap 0.14/0.11

T/N cable swap 0.16/0.13

S/N cable swap 0.43/0.37

At what rate can you buy cable for value tomorrow?

Question125: What would be the strategy for a bank if it is unable to speculate on interest rates and/or unable to absorb market risk?

Question126: The Model Code strongly recommends that intra-day oral deal checks should:

Question127: Which one of the following formulae is correct?

Question128: You are quoting forward FX prices to a broker subject to finding a counterparly for a matching transaction.

The Model Code says:

Question129: Which of the following are all goals of the originator of securitized assets?

Question130: A dealer in the spot foreign exchange market has to assume that a price given to a voice broker is only valid:

Question131: What should a broker do if his quoted price is hit simultaneously by several dealers for a total amount greater than that for which the price concerned was valid?

Question132: What is the probability of an at-the-money option being exercised?

Question133: Extended trading hours and off-premises dealing can involve additional hazards, the avoidance of which requires clear controls. The Model Code prescribes best market practice. Which of thefollowing is true?

Question134: You have quoted your customer the following CAD deposit rates:

1M 1.00-05%

2M 1.06-11%

3M 1.13-18%

The customer says, "I give you CAD 20,000,000.00 in the two's". What have you done?

Question135: The outright forward FX rate is not a function of which of the following?

Question136: From 2019 on the total capital requirement for banks under Basel III will be defined as:

Question137: Gambling or betting amongst market participants has obvious dangers and:

Question138: What happens when a coupon is paid on bond collateral during the term of a sell/buy-back?

Question139: The buyer of a USD/ARS NDF could be:

Question140: What is replacement cost a function of?

Question141: Which one of the following statements about claims is true?

Question142: When an employee executes a personal trade in advance of a client's or institution's order to benefit from the anticipated movement in the market price following the execution of a large trade, it is called:

Question143: The Model Code recommends that when banks accept a stop-loss order

Question144: You are quoted spot NZD/USD 0.6821-26 and USD/CHF 1.4652-56 at what price can you buy CHF against NZD?

Question145: Today is Monday, 8th December. You sell a 9x12 USD FRA for value Thursday, 10th September next year. On what date is the settlement amount due to be paid or received (assuming that there are no holidays)?

Question146: What is the day count/annual basis convention for euroyen deposits?

Question147: Under what conditions can an FX broker act as a position taker?

Question148: What does the Model Code recommend in respect of prices and orders made on electronic trading platforms?

Question149: A forward/forward FX swap:

Question150: Payment and settlement instructions should be passed:

Question151: The market is quoting:

1-month (31-day) USD. 1.75%

3-month (91-day) USD. 2.05%

What is the 1x3 rate in USD?

Question152: The market is quoting:

1-month (31-day) NOK 1.75¡ãk

3-month (91-day) NOK 2.05%

What is the 1x3 rate in NOK?

Question153: Principals are allowed to:

Question154: A customer sells a LIFFE Euro Swiss futures contract. Which of the following risks could he be trying to hedge?

Question155: Which of the following statements is correct?

Question156: The term "under reference" refers to:

Question157: Management policy on the use of mobile devices by trading sales and settlement staff should:

Question158: An FRA is:

Question159: A broker offers a dealer an incentive in the form of a reduction to the agreed schedule of brokerage between the firms.

Question160: Which of the following is true?

Question161: What is a Vostro account?

Question162: Using reprising gap analysis, a bank's balance sheet is considered liability-sensitive to market interest rate changes, if:

Question163: How can material divergences between the value of cash and collateral be managed in a documented sell/ buy-back?

Question164: What is the buyers primary risk in a repo?

Question165: If the daily 90% confidence level VaR of a portfolio is correctly estimated to be USD 5,000.00, one would expect that:

Question166: What are de minimis claims?

Question167: If USD/JPY is quoted to you as 98.10-15 and USD/CHF as 0.9294-99, what is the rate at which you can buy CHF against JPY?

Question168: The organisational structure of market participants should ensure a strict segregation between front and back office of:

Question169: Which of the following risks are considered market risks?

Question170: When initially negotiating an interest rate swap, a principal indicated his intention to assign it to a third party. In executing such a transfer:

Question171: Which one of the following statements about mark-to-model valuation is correct?

Question172: Which of the following statements about requirements for limit setting is correct?

Question173: The major difference between futures and OTC instruments like FRAs and interest rate swaps is that futures are:

Question174: You have received a gift from a good friend who also happens to be your USD/YEN broker. Under such circumstances, the Model Code recommends that you should:

Question175: A bank quotes 3-month EUR deposits at 0.45% ¡ª 0.55% to its broker. The broker lifts the bank's offer at

0.55%. Which of the following steps must the broker take?

Question176: A CD with a face value of USD 250,000,000.00 was issued at par with a coupon of 5% for 91 days.

You buy it in the secondary market when it has 30 days remaining to maturity and is trading at

5.25%. How much do you pay?

Question177: If you buy GBP 2,000,000 against USD at 1.6020; GSP 1,000,000 at 1.6035 and GBP 3,000,000 at

1.6028, what is the average rate of your position?

Question178: The intrinsic value of a long call option:

Question179: The market is quoting:

1-month (30-day) GBP 0.47%

7-month (213-day) GBP 0.74%

What is the 1x7 rate in GBP?

Question180: How much is a big figure worth per million of base currency it EUR/GBP is 0.6990?

Question181: Brokers should confirm all transactions:

Question182: Under Basel rules, what is the meaning of RWA?

Question183: You want to hedge your deposit against falling interest rates. Which of the alternatives below are appropriate for this purpose?

Question184: Bank XYZ calls you for a quote in EUR/USD for EURO 20 million. If you decide to quote to Bank XYZ:

Question185: The extension of forward FX contracts at their historic rates is only allowed when:

Question186: How is an outright forward FX transaction quoted?

Question187: If you take an 18-month USD deposit, when is interest payable?

Question188: Which of the following are transferable instruments?

Question189: Which of the following definitions of a nostro account is correct?

Question190: You have made a price by a Japanese bank in (SD 2,000,000.00 against JPY. They made you

98.95-03 and you took the offer. USD/JPY is now quoted 98.78-81 and you square your position.

What is your profit or loss?

Question191: What is the name of a swap in which the counterparties sell currencies to each other with a concomitant agreement to reverse the exchange of currencies at a fixed date in the future at the same price, and where the interest rates for the two currencies are reflected in the two exchanges but paid separately?

Question192: When differences in payment arise because of errors in the payment of funds:

Question193: Which of the following dealing strategies involves the placing of orders with very short quote lives into a market?

Question194: You are paying 1,00% per annum paid semi-annually and receiving 6-month LIBOR on a USD

10,000,000.00 interest rate swap with exactly two years to maturity. 6-month LIBOR for the next payment date is fixed today at 0.95%. How would you hedge the swap using FRAs?

How to hedge an IRS with a strip of FRAs?

Question195: When performing a gap analysis, into which of the following time buckets should a 5-year floating-rate note with a 6-month LIBOR coupon be slotted?

Question196: Which of the following statements regarding economic capital is correct?

Question197: What kind of information should dealers and brokers take care when relaying?

Question198: Written confirmation is a function that can be done by:

Question199: A 7-day piece of USCP is quoted at a rate of discount of 1.75%. What is its true yield?

Question200: Today's date is Thursday 12th December. What is the spot value date? Assume no bank holidays.

Question201: How many Yen would you pay to buy 1 ounce of gold if you were quoted the following?

XAU/USD 1575.25-75

USD/JPY 96.55-60

Question202: The delta of an 'at-the-money' long put option is:

Question203: Risk capital is intended to ensure that an institution can:

Question204: To curb attempted fraud, banks should:

Question205: When is interest conventionally due on a 3-year interbank eurodollar deposit?

Question206: Which of the following statements reflects the position of the Model Code on gambling or betting amongst market participants?

Question207: Which of the following is issued by auction?

Question208: The use of mobile phones within the dealing room is not considered good practice except

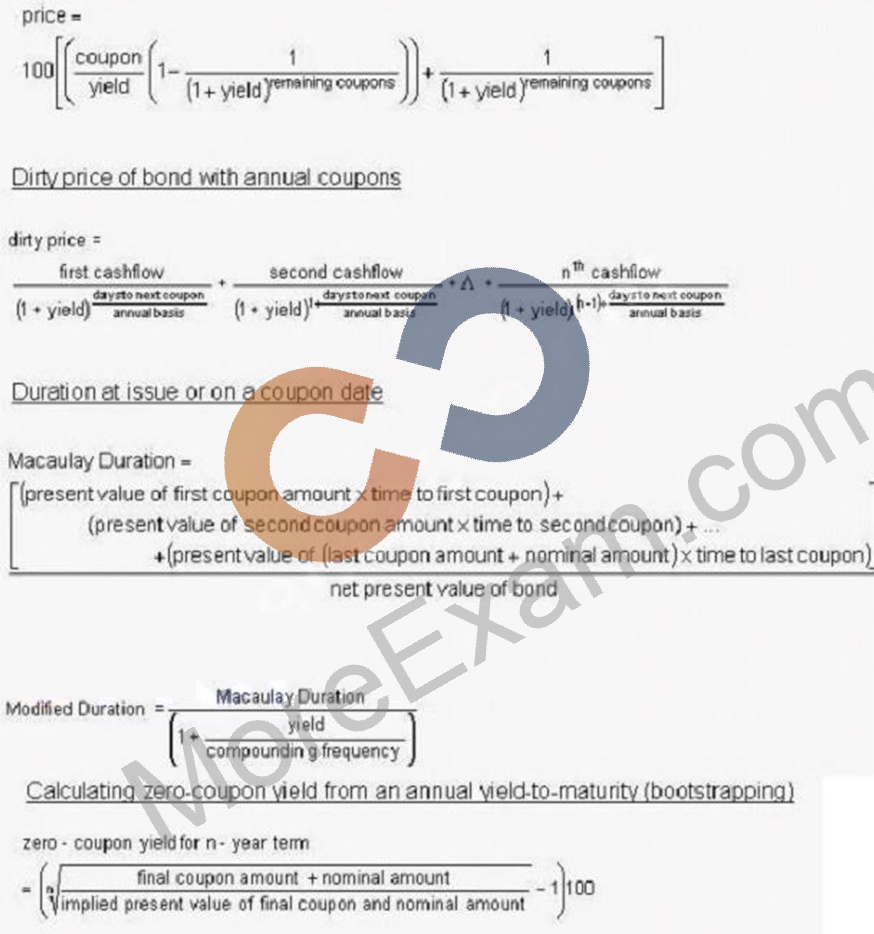

Question209: Which of the following statements is correct regarding duration?

Question210: If several banks hit a broker simultaneously for an amount greater than the amount for which the price was shown:

Question211: You bought a USD 4,000000 6x9 FRA at 6.75%. The settlement rate is 3-month (90-day) BBA LIBOR, which is fixed at 5.50%. What is the settlement amount at maturity?

Question212: The Model Code stipulates that you have a right to qualify your quotes in terms of amounts:

Question213: Which of the following statements is true? The repo legal agreement between the two parties concerned should:

Question214: You buy a 181-day 2.75% CD with a face value of USD 1,500,000 at par when it is issued. You sell it in the secondary market after 150 days at 2.60%. What is your holding period yield?

Question215: You are the buyer of protection in a credit default swap. All other things being equal your counterparty credit risk is increasing if:

Question216: Under Basel III rules the meaning of RSF is:

Question217: Is gambling or betting between market participants allowed?

Question218: Net funding requirements in liquidity management are determined by means of:

Question219: You have quoted a Swiss customer spot USD/CHF as 0.9273-78, but he asks you to quote it as CHF/USD.

What do you quote?

Question220: A sold JUN 3-month STIR-future should be reported in the gap report as of 22 May:

Question221: Which of the following pays a return in the form of a discount to face value?

Question222: For which country's currency is SEK the ISO code?

Question223: The Liquidity Coverage Ratio imposed by Basel III requires a bank:

Question224: Under new Basel rules, what is the meaning of CVA?

Question225: In case of a default on a repo by the seller:

Question226: In all dealing conversations, the Model Code strongly recommends:

Question227: The columns below list short-term cash rates on 3rd April and 3rd F1ay 3rd April 3rd May

Describe the shape of the short-term segment of the yield curve on 3' April using market terminology. In addition, describe the change in the shape of the curve between 3rd April and 3rd May.

Question228: What is the ISO code for the Indian rupee?

Question229: What does the Model Code say about netting?

Question230: You bought USD 5,000,000 against EUR at 1.1037 and 3,000,000 at 1.1052. If the EUR/USD rate is now quoted 1.1015/17, and it you deal at that rate, what profitwould you make?

Question231: What does the term "mine" mean when given in response to an FX spot quotation?

Question232: What type of institution is the typical issuer of bank bills?

Question233: Convert 8.25% quoted on a semi-annually compounded money market basis for USD to the equivalent annually-compounded bond basis.

Question234: In a plain vanilla interest rate swap, the "fixed-rate payer":

Question235: When a broker calls "off" at the very instant a dealer "hits" the broker's price:

Question236: A dealer has indicated his intention of assigning an interest rate swap to a third party soon after transacting that swap. When about to execute an assignment

Question237: If a dealer has any intention of assigning an interest rate swap to a third party soon after transacting that swap:

Question238: Making interest rate swap transactions subject to agreement on documentation:

Question239: The Model Code rules that deals at non-current rates:

Question240: If I say that I have "bought and sold" EUR/USD in an FX swap, what have I done?

Question241: You are the fixed-rate payer in a plain vanilla interest rate swap. If your counterparty defaults, your exposure at default is:

Question242: What is a "normal" shaped curve?

Question243: The mid-rate for USD/CHF is 1.3950 and the mid-rate for AUD/USD is 0.7060. What is the midrate for CHF/AUD?

Question244: Once a prime-broker has matched and accepted a trade, separate confirmations must be exchanged between:

Question245: From the following GBP deposit rates:

1M (31-day) GBP deposits 3.15%

2M (61-day) GBP deposits 3.25%

3M (91-day) GBP deposits 3.41%

4M (120-day) GBP deposits 3.56%

5M (152-day) GBP deposits 3.73%

6M (182-day) GBP deposits 3.90%

calculate the 3x4 forward-forward rate.

Question246: The interest earned on a USD 5,000,000.oo money market deposit for 184 days is USD 12,500.00. What was the interest rate?

Question247: The delta of an at-the-money long call option is:

Question248: Three of the following non-EU countries have unilaterally adopted the Euro. Which one has not?

Question249: An option premium is a positive function of:

Question250: Which of the following does the Model Code not recommend to prevent technical errors by etrading devices?

Question251: When quoting the exchange rate between the EUR and AUDI which is conventionally the base currency?

Question252: What usually happens to the collateral in a tri-party repo?

Question253: What is the principal risk identified by gap management reporting?

Question254: If EUR/USD is quoted to you as 1.3030-40 and GBP/USD as 1.5320-30, at what rate can you sell GBP and buy EUR?

Question255: A customer gives you GBP 25,000,000.00 at 0.625% same day for 7 days.

Through a broker, you place the funds with a bank for the same period at 0.6875%.

Brokerage is charged at 2 basis points per annum.

What is the net profit or loss on the deal?

Question256: What is settlement risk in FX?

Question257: You quote the following rates to a customer spot GBP/CHF 2.2005-10

3M GBP/CHF swap 120/115

At what rate do you sell GBP to a customer 3-month outright?

Question258: If EUR/USD is quoted to you as 1.1050-53, does this price represent?

Question259: If you sell forward USD to a client against EUR, what is the first thing you should do to cover your exposure to exchange rate movements?

Question260: In trade confirmation, which one of the following statements about "matching" is correct?

Question261: Which of the following will tend to have the higher yield?

Question262: Which of the following is the best description of a "broken trade"?

Question263: What rates should a panel bank contribute to the EURIBOR fixings?

Question264: What does the Model Code recommend regarding the practice of "name switching/substitution"?

Question265: Using the following rates:

Spot GBP/CHF 1.4235-55

Spot CHF/SEK 6.8815-45

3M GBP/SEK swap 140/150

What is the price for 3-month outright GBP/SEK?

Question266: Claims should be communicated in writing via e-mail or preferably by authenticated SWIFT. What information should be provided in the claim?

Question267: If you lend for 3 months and borrow for 6 months, you may be said to:

Question268: The one-month (31-day) GC repo rate for French government bonds is quoted to you at 3.75-80%. As collateral, you are offered EUR25 million nominal of the 5.5% OAT April 2006, which is worth EUR

28,137,500. If you impose an initial margin of 1%, the Repurchase Price is:

Question269: The major difference between FRAs and futures is that FRAs are:

Question270: What is the effect of netting?

Question271: The market is quoting:

3-month (90-day) NZD 2.55%

6-month (182-day) NZD 2.75%

What is the 3x6 rate in NZD?

Question272: If you have created a 'synthetic asset' by buying and selling a USD/CHF swap, what have you done?

Question273: You are the buyer of a receiver's swap. All other things being equal your counterparty risk is increasing if

Question274: A closed position in a particular foreign currency exists:

Question275: Which of the following correctly states the Model Code's recommendations regarding terms and documentation?

Question276: Today is Monday, 8th December. You sell a 9x12 FRA for value Thursday, 10th September next year. On what date is the settlement amount due to be paid or received (assuming that there are no holidays)?

Question277: The Interest Rate Parity Theorem states that:

Question278: What should be done when a voice broker calls "off" at the very instant the dealer hits the broker's price as

"mine" or "yours"?

Question279: Where repos or securities lending transactions are entered into, the Model Code recommends:

Question280: A USD deposit traded in London between two German banks is cleared:

Question281: You have just sold USD 5,000,000.00 spot against JPY. What type of risk does not apply?

Question282: What is an FX swap?

Question283: What is a master agreement intended to do?

Question284: Dealers are allowed to trade for their own account only if:

Question285: Brokers shall not reveal the identity of a counterparty unless:

Question286: How many USD would you have to invest at 3.5% to be repaid USD125 million (principal plus interest) in

30 days?

Question287: Your are quoted the following rates:

spot CHF/JPY 60.12-22

3M CHF/JPY 25.5/22.5

At what rate can you buy 3-month outright JPY against CHF?

Question288: You have bought a 93-day US Treasury bill at 5.63%. What is the true yield?

Question289: All prices quoted by brokers should be taken to be:

Question290: Which of the following currencies is quoted on an actual/360 basis?

Question291: Which of the following statements is correct?

Question292: How is an outright forward FX transaction quoted?

Question293: Using the following rates:

spot GBP/CHF 2.3785-15

spot CHF/SEK 5.5975-85

3M GBP/SEK swap 725/690

What is the price for 3-month outright GBP/SEK?

Question294: If GBP/USD is quoted to you at 1.6120-30, how much GBP would you receive if you sold USD

2,000,000.00?

Question295: The Model Code recommends that, in the case or complaints about transactions, management should:

Question296: When a broker needs to switch a name this should be done:

Question297: Which of the following statements about requirements for dealing with limit violations is correct?

Question298: If the yield curve is upward sloping, a bank would not profit from:

Question299: Which of the following is not in the Model Code?

Question300: You hear from a client of good standing that a major market participant has taken major losses on its proprietary trading book and is desperate for liquidity. You are not convinced that the story is true, but have a friend at another bank who you know has very large exposures to this firm and would be seriously damaged by a default. What advice does the Model Code give?

Question301: On fixing date, the settlement payment of an NDF reflects the differential between the agreed forward rate and:

Question302: Which of the following statements about "standard settlement instructions" (SSI) is correct?

Question303: Which of the following both provide credit enhancement to a true-sale securitization?

Question304: Which of the following is true regarding the consummation of a deal?

Question305: What is the London Gold Price Fix (London Gold Fixing)?

Question306: If the duration gap is zero, how will a small parallel shift in interest rates affect the market value of the bank's equity?

Question307: When can a broker consider a deal to be done?

Question308: A 3-month (90-day) NZD deposit is 2.75% and 6-month (180-day) NZD deposit is 3.00%. What is the 3x6 NZD deposit rate?

Question309: Any breaches in confidentiality should be:

Question310: Which one of the following statements is incorrect under Basel III?

Question311: Deliberately inputting incorrect big figures into an electronic dealing platform is:

Question312: A CD with a face value of USD 50,000,000.00 and a coupon of 4.50% was issued at par for 90 days and is now trading at 4.50% with 30 days remaining to maturity. What has been the capital gain or loss since issue?

Question313: You have quoted your customer the following eurodollar deposit rates:

1M 5.375-25%

2M 5.4375-3125%

3M 5.5-375%

The customer says, "I give you USD 20 million in the two's".

What have you done?

Question314: If you funded your fixed-income investment portfolio with short-term deposits, how would you hedge your interest rate exposure with interest rate swaps?

Question315: A dealer needs to buy USD against SGD. Of the following rates quoted to him, which is the best rate for him?

Question316: Which one of the following statements regarding the variance-covariance method for calculating value-at- risk is true?

Question317: What is the value date of a 6-month outright forward FX transaction dealt today, if today's spot date is Monday, 30th June? Assume there are no bank holidays.

Question318: Click on the Exhibit Button to view the Formula Sheet, If GBP/USD is 1.5350-53 and USD/JPY is 106.50-

53, what is GBP/JPY?

Question319: An interest rate guarantee (IRG) is:

Question320: Cable is quoted at 1.6075-80 and you say "5 yours!" to the broker. What have you done?

Question321: A 6-month SEK/NOK Swap is quoted 140/150. Spot is 0.9445. Which of the following statements is correct?

Question322: Dealers should not conduct dealing activities outside the bank unless:

Question323: Which of the following is not true?

Question324: Where dealing through an intermediary with an unidentified principal, the Model Code recommends:

Question325: A forward-forward loan creates an exposure to the risk of:

Question326: Under Basel Securitization rules the highest potential risk weight is:

Question327: Forward points represent:

Question328: In dealing terminology, what does "my risk" refer to?

Question329: You are paying 5% per annum paid semi-annually and receiving 6-month LIBOR on a USD 10 million interest rate swap with exactly two years to maturity . 6-month LIBOR for the next payment date is fixed today at 4.95%. You expect 6-month LIBOR in 6 months to fix at 5.25%, in 12 months at 5.35% and in 18 months at 5.40%. What do you expect the net settlement amounts to be over the next 2 years? Assume

30-day months.

Question330: What are 1MM dates?

Question331: Which of the following statements about Credit Default Swaps (CDS) is correct?

Question332: A negative yield curve is one in which:

Question333: Does the slope of the interest yield curve typically have a substantial impact on a bank's net interest margin?

Question334: You have written a EUR/USD knock-in option for a bank counterparty. At 6pm New York time on Friday, the instrike point is breached. This is confirmed on screens. The counterparty contacts you to confirm that the option has been knocked in.

Question335: Under Basel rules, what is the meaning of IRB?

Question336: Banks have a fiduciary responsibility to ensure that clients have all necessary information to understand the transaction because this:

Question337: In spite of having agreed to a deal, dealers are not bound to its terms if it is "subject to documentation".

What position does the Model Code take with regard to this practice?

Question338: Confirmations should be sent out by both counterparties through an efficient and secure means of communication, preferably electronic:

Question339: The two-week repo rate br the 5.25% bund 2007 is quoted to you at 3.33-38%. You agree to reverse in bonds worth EUR 266,125,000 with no initial margin. You would earn repo interest ot

Question340: Which of the following is part of the typical scope of Asset Liability Management (ALM)?

Question341: For which of the following reasons is the extension of forward contracts at non-current rates is discouraged:

i. These could be used to conceal profit or losses.

ii. These could be used to perpetrate fraud.

iii. These could result in an unauthorised extension of credit.

iv. These could result in confusing settlement instructions.

Question342: An FX forward outright has been dealt for a value date which is subsequently declared to be a bank holiday. According to the Model Code, the exchange rate for the deal:

Question343: An option contract that gives the buyer the right to exercise the option at several distinct points during its life is called:

Question344: In spite of having agreed to a deal, dealers are not bound to the deal if it is subject to documentation. The Model Code:

Question345: Which of the following are quoted in terms of a discount rate?

Question346: Which of the following is a Model Code good practice regarding the passing of names?

Question347: Which of the following currencies is quoted on an ACT/365 basis for the calculation of interest on interbank deposits in London?

Question348: A transaction that entails market price risks may be entered into in the absence of a market price risk limit...

Question349: Taking collateral to hedge the credit risk on a counterparty means that you have:

Question350: When would an exporter commonly use an NDF?

Question351: At the end of the day, you are short CHF 3,500,000.00 against SEK at 6.9275. You are asked to revalue your position at 6.9190. What is the resulting profit or loss?

Question352: How can material divergences between the value of cash and collateral be managed in a documented sell/ buy-back?

Question353: What is the Gold Offered Forward Rate (GOFO)?

Question354: All other things being equal the interest rate risk of a fixed coupon bond is:

Question355: You are paying 5% per annum paid semi-annually and receiving 6-month LIBOR on a USD 10 million interest rate swap with exactly two years to maturity. 6-month LIBOR for the next payment date is fixed today at 4.95%. How would you hedge the swap using FRAs? How to hedge an IRS with a strip of FRAs?

Question356: What does the Model Code say concerning repos and stock-lending?

Question357: The 180-day CAD/CHF rate is bid 62 and the 90-day CAD/CHF rate is bid 29. What is the bid rate for 120 days, assuming straight-line interpolation?

Question358: What is the risk of dealing through an agent with an unknown principal?

Question359: What is the incentive for market-making?

Question360: You need to buy USD 5,000,000 against GBP and are quoted the following rates concurrently by two separate banks: 1.6045-50 and 1.6047-52. At which rate do you trade?

Question361: You have prepared the following economic capital table for the next ALCO meeting:

For which of the following risks should you consider actions?

Question362: What do you call a combination of a long (short) call option and short (long) put option with same face value, same expiration date, same style, where the strike price is equal to the forward price?

Question363: Which of the following statements is false? The repo legal agreement between the two parties concerned should:

Question364: The maturity of a straight 3-months deposit falls on Saturday, which happens to be the last day of the month. What is the actual deposit maturity date?

Question365: You have quoted a Swiss customer spot USD/CHF as 1.3710-15, but he asks you to quote it as CHF/USD.

What do you quote?

Question366: USD/CHF is quoted to you at 0.9290-93 and GBP/USD at 1.5320-30. At what rate could you buy GBP and sell CHF?

Question367: In order to be introduced in a controlled manner, which areas should be involved before a new product or business strategy is launched?

Question368: Under what circumstances are banks allowed to "park" deals or positions with a counterparty?

Question369: 3-month USD/CHF is quoted at 12/10. Interest rates in Switzerland are reduced but USD rates (which are higher) are unchanged. What would you expect the 3-month forward USD/CHF rate to be?

Question370: To establish and maintain a short position in deliverable securities, you must:

Question371: Which one of the following bullion coins has a 999.9/1000 gold purity (.9999 fineness)?

Question372: What is the major difference between a CD and a deposit?

Question373: Which of the following statements reflects the Model Code on gambling or betting amongst market participants?

Question374: Click on the Exhibit Button to view the Formula Sheet, If the value date of forward USD/JPY transactions is declared a holiday in either New York or Tokyo, the correct value date will be:

Question375: If spot AUD/USD is quoted to you as 0.7406-09. How many AUD would you receive in exchange for USD

5,000,000 if you dealt on the price?

Question376: What is the expression used to describe a genuine error (wrong amount, wrong side, wrong rate) made by a dealer in the execution of an order on an electronic platform?

Question377: Assume the following scenario:

Bank A bids for EUR 5,000,000.00 at 1.3592.

Bank B offers EUR 10,000,000.00 at 1.3597.

Broker XYZ quotes to the market EUR/USD 1.3592/97.

Bank C takes the offer at 1.3597.

What information is the broker obliged to reveal?

Question378: Which one of the following statements about "CLS rescinds" is correct?

Question379: If a 12-month AUD/NZD swap is quoted 53/47, which of the following statements would you consider to be correct?

Question380: Bank participants have a duty to make it clear that their prices are firm or merely indicative:

Question381: It is now permissible in most markets for brokers to be owned by banks and other principals. Where there is shared management, or a share holding or other investment in a broker by a counterparty:

Question382: The rho of an option is:

Question383: An 'at-the-money' call option:

Question384: Which of the following statements about operational risk awareness is correct?

Question385: As to the Charter of ACI - The Financial Markets Association, what do members not pledge?

Question386: When is interest conventionally due on a 3-year interbank EUR deposit?

Question387: You are a sales person in a bank and are about to sell a structured note to a non-professional customer.

Before finalizing the transaction you remember to double-check the customer's charter. You learn that the customer is not allowed to invest in structured products. The risk you have avoided is most likely to be classified as:

Question388: What is Funds Transfer Pricing in the ALM process?

Question389: When you are accepting a stop loss order, you must:

Question390: Which of the following risks is best mitigated by CLS?

Question391: How is a USD Overnight Indexed Swap (OIS) settled?

Question392: You deal over the phone with a counterparty. The subsequent confirmation differs from the terms agreed verbally. What is the result?

Question393: Which SWIFT message should be used to advise the netting position of a currency resulting from FX, NDF, options and other trades?

Question394: What is the ISO code for the Lebanon pound?

Question395: What is meant by "short dates"?

Question396: The torward points are calculated from:

Question397: All other things being equal, if a bank borrows short and lends long what is the effect on the liquidity risk of the bank?

Question398: Four banks provide you with quotes in CHF/SEK. Which is the best price for you to buy SEK?

Question399: Which of the following statements about the Liquidity Coverage Ratio is correct?

Question400: You are quoted the following market rates:

Spot EUR/USD 1.3097-00

0/N EUR/USD swap 0.08/0.11

TIN EUR/USD swap 0.29/0.34

S/N EUR/USD swap 0.10/0.13

Where can you buy EUR against USD for value tomorrow?

Question401: The popularity of FX-trading via Internet platforms has serious implications for the applicability of traditional rules such as "Know Your Customer". Which of the following are correct?

Question402: If there is a need for assistance to help resolve a dispute over differences between a broker and a bank, the Model Code suggests turning to:

Question403: What is an outright forward FX transaction?

Question404: A 3-month (91-day) deposit of EUR25 million is made at 3.25%. At maturity, it is rolled over three times at

3.55% for 90 days, 4.15% for 91 days and 4.19% for 89 days. At the end of 12 months, how much is repaid (principal plus interest)?

Question405: If a broker refers to "the payer of 5-year euro at 4.12", what is this party doing?

Question406: You borrow GBP 2,500,000.00 at 0.625% for 165 days. How much do you repay including interest?

Question407: When quoting the exchange rate between the USD and AUDI which is conventionally the base currency?

Question408: Where the Committee for Professionalism of the ACI has been notified of a breach of the letter or spirit of the Model Code, it

Question409: What is the maximum maturity of a US Treasury bill?

Question410: Are the forward points materially affected by changes in the spot rate?

Question411: Who typically communicates the bank's asset and liability management policy internally?

Question412: The Model Code's correct recommendation regarding electronic trading states:

Question413: If GBP/USD is 1.5350-53 and USD/JPY is 97.50-53, what is GBP/JPY?

Question414: The premium on an option contract is:

Question415: Mark-to-market' in a repo means: